On examination, fiat and shitcoins share the same trick of getting people to give up real value for promises.

This is an opinion editorial by Joakim Book, a Research Fellow at the American Institute for Economic Research, and writer on all things money and financial history.

All (fiat) monies struggle with getting their users to hold the liabilities of their issuer. Put differently, only issuers with some degree of trust or credibility manage to “monetize” some part of their debts, by literally having others carry it for them for free. In the extreme, it means that the issuer gets a perpetual, non-redeemable, interest-free loan with which it can finance a portfolio of assets — the profits of which they may spend as it pleases. The most well-known instance of this is the Federal Reserve Board, and its .

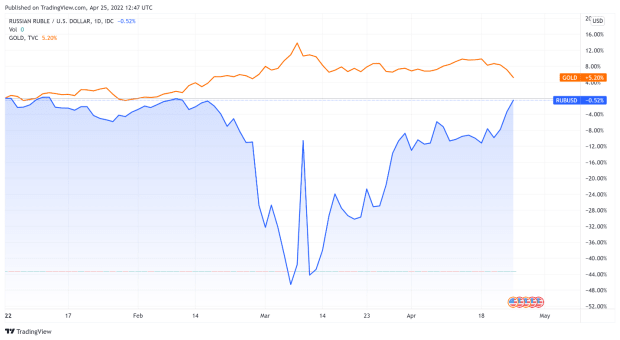

Since the gold announcement, the ruble has recovered the level it held against USD before the Ukraine invasion. Did the gold-backing stunt therefore work?

More likely, this was all a quick-fix credibility play, making the ruble somewhat more desirable for others to hold — if only briefly for transactional purposes. For The Financial Times, Robin Wigglesworth summarizes: “Imports have been crushed, interest rates have been doubled, harsh capital controls have been put in place, and Russia’s oil and gas sales means it continues to accumulate foreign earnings.” No wonder the ruble trades higher on a much smaller market.

Besides:

- Gold standards operate on trust: and nobody trusts Vladimir Putin, so it’s very unlikely that this would do much.

- The ruble-gold play still lacks the redeemability feature that makes for true outside money. Depositors of, say, BlockFi can redeem their BTC deposits into sats; depositors of, say, Bank of America, can withdraw bank money into outside-money cash notes. Holders of rubles can … not do anything. Redeem them for gold …?

All currencies fight for liquidity and one tool they use in that fight is offering reasons for their users to hold their debt or token. In that sense, the plethora of shitcoins aren’t that different from the ruble, its issuer desperately trying to shore up fake demand and limit outflows from its monetary network. Levine again:

“… people mostly don’t trust the dollar because you can earn 100% interest on dollars, or even because you can earn a small amount of interest on dollars; they trust the dollar because they trust the dollar, in a circular, widespread-social-adoption sort of way. You don’t need to end up with a Ponzi scheme.”

It’s hard to tell where the ruble, freed of internal capital controls and foreign sanctions, would trade against the USD. And it’s hard to stipulate where fiat currencies would trade against hard assets like gold or bitcoin were they freed of government control and taxation.

The circularity of monetary demand is what all currencies aspire to, and the Central Bank of Russia has recently shown us some of the shitcoin tools it wields. The Russian currency may be one step up in respectability from shitcoinery, but it’s shitcoinery nonetheless. In contrast to many of its digital rivals, it has large supplies of commodities, natural gas and gold supplies that it can use to defend its token or engineer monetary demand for it — not to mention an army, a bureaucracy and a tax system.

The sociolinguist Max Weinreich is supposed to have quipped that “A language is a dialect with an army.”

We could say the same about shitcoins and fiat currencies.

This is a guest post by Joakim Book. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc. or Bitcoin Magazine.