A recent column by the Financial Times’ Jemima Kelly demonstrated some misunderstandings about Bitcoin’s decentralization and singularity.

This is an opinion editorial by Stephan Livera, host of the “Stephan Livera Podcast” and managing director of Swan Bitcoin International.

Financial Times Columnist Jemima Kelly published an article titled “Don’t Believe The ‘Maximalists: Bitcoin Can’t Be Separated From Crypto” earlier today and I’d like to share some reactions from a Bitcoiner perspective. Quoted text below is all from Kelly’s article.

“If you have ever dared to direct criticism at the world of crypto, the chances are you will have received some charming rebukes. You are likely to have been told to ‘have fun staying poor’…”

For what it’s worth, I believe the “have fun staying poor” meme is mostly meant in jest and not a serious statement of ill intent towards another person. Why? Because we popularly saw Bitcoiners telling Elon Musk, the richest man in the world at the time, to “have fun staying poor” as he backs away from his public support of Bitcoin. Clearly, this is not meant as a serious rebuke.

“But there is another slightly more sophisticated flavour of counter-criticism finding its way into my inbox with increasing regularity these days. It usually starts with something designed to appease — some kind of agreement that crypto is immoral, a scam, or some version of a Ponzi scheme. But then it quickly changes course, to explain that none of this applies to bitcoin.”

Here is where my principal disagreement with this article lies. I and many other Bitcoiners do believe that we should draw a line of distinction between Bitcoin and “crypto.” Bitcoin is unique in many ways:

- It has no pre-mine or “dev. tax” to enrich the founder or founding team.

- It has a culture that actually prioritizes decentralizing the ecosystem.

- It enables cheap blockchain validation and participation (i.e., it’s relatively easy to run a fully-validating Bitcoin node), while also maintaining a robust, open, scalable, trust-minimized system.

- It has a very strong preference for soft forking and retaining backwards and forwards compatibility for those running older Bitcoin node software.

- It is continually growing in acceptance and mindshare around the world. Of course, this does wax and wane with bull and bear markets, but zoomed out, bitcoin liquidity and acceptance is only going one way: up.

Once you genuinely explore these points, you will find that only Bitcoin meets these criteria. Many altcoins regularly hard fork, which is an indicator that they have a certain level of centralization in their development and community. Other altcoins do things that simply would not be scalable if they were scaled up to the level of Bitcoin and the number of bitcoin transactions. Other altcoins do things that are more permissioned, and thus they are not an open system like Bitcoin is.

You might even argue that a specific altcoin does one specific thing better than Bitcoin does, but are any of them meaningfully making improvements on the whole? I don’t think so, and that’s why Bitcoin is rightly in a category of its own. There is also the question of whether Bitcoin should have these supposed other features or things, as this may also cause negative trade offs in one of the other worthwhile qualities of the system (robustness, decentralization, scalability, verifiability, etc.).

Kelly seems to believe that Bitcoin “arguments don’t stand up,” as she takes issue with any financial incentive whatsoever. For instance:

“First, it doesn’t matter what bitcoin’s origins were — the people who push it now have the same financial incentives as those pushing any other crypto token.”

How is this a justified attack on Bitcoin promotion? Imagine that you are an investor in a company, and you openly promoted that company without hiding the fact that you are an investor. Is there an issue with this?

Now, imagine that there are fraudulent competitors that purport to be “in the same industry.” You advocate for people to use the product of your non-fraudulent company instead. Where is the ethical issue? How would this “disprove” you? It simply doesn’t, unless you’re clutching at straws.

Of course, Bitcoin is not a company. But in any case, the promise of Bitcoin is not that “there were no people who got in cheaper than you,” which is an absurd and impossible standard to live up to. The promise of Bitcoin is an open, decentralized, scarce, robust, programmable monetary system with no rulers. The product does what it proverbially says on the tin and Kelly’s critique falls flat.

“Second, bitcoin is not in fact decentralized — not only do miners group together to form ‘mining pools’ but wealth is also hugely concentrated.”

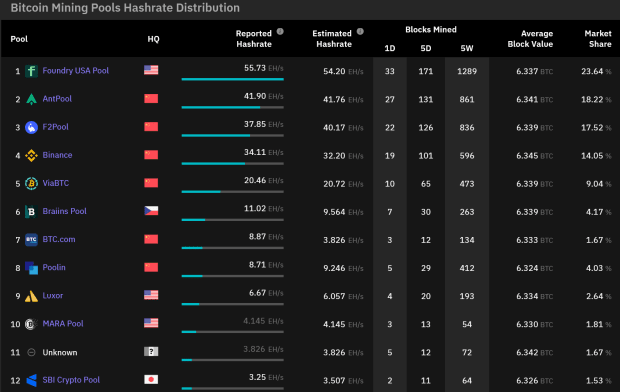

Kelly is not correctly summarizing the relationship between miners and pools. Miners are distinct entities from pools, and they can re-point their hash rate to a different pool quickly. And so while there may be comparatively a smaller amount of pools, individual miners can and do switch between them, as it is a brutally competitive market. See this screenshot as of September 23, 2022 from the Braiins Insights Dashboard, which shows how pools are headquartered in different countries around the world:

Also topical is the recent Poolin news, that saw the company suspend withdrawals. Given this, a lot of miners pointed their hash rate away from Poolin. Notice how Poolin’s global share of bitcoin mining hash rate has gone from 12% previously, down to around 4% at the time of writing.

“On Tuesday, MicroStrategy announced that it had bought another 301 bitcoins, meaning this company alone now holds almost 0.7 per cent of the entire supply.”

Kelly claims to “steelman the argument” in this article, but unfortunately, she does a poor job steelmanning on the question of bitcoin ownership. If she grasped the libertarian and cypherpunk ethos of Bitcoin, she would understand that the point is to create a monetary system without coercing people into it. So, of course given this, there will be some people who get it before others do. Those who get it will buy, earn or mine coins before others do. The fact that one company owns 0.7% of the circulating supply of bitcoin is not an issue.

So, Bitcoin remains far more decentralized than the “crypto” coins.

“Third, a ‘first-mover advantage’ does not always last.”

That’s true in a general business context, however to understand why Bitcoin is distinct, we have to understand just why and how far it beats alternatives, be they fiat money, gold or altcoins. Generally, in order to displace another product, you have to come up with something ten times better. But with Bitcoin, it’s doubtful that ten times better is even possible. Here, I’ll quote my friend Gigi in his recent Twitter thread:

The design space of money is limited, and a ten-fold improvement on the monetary properties of Bitcoin is simply not possible. You can marginally improve one thing, but only by dramatically worsening trade-offs in other ways (verifiability, scalability, robustness, accessibility).

Kelly then writes again about the incentive of Maximalists:

“The real reason bitcoin maximalists want to separate bitcoin from the rest of crypto is to create the illusion of scarcity in a world where there is none.”

It’s fair to say that Bitcoin Maximalists have an incentive and want to distinguish bitcoin from “crypto.” But the real question is: Are they right? Yes, they are.

Bitcoin is rightly distinguished from altcoins, but it just takes a lot of research and reading to understand why. Unfortunately, Kelly has not done the research required and presents only a shallow surface level misunderstanding.

This is a guest post by Stephan Livera. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.