Too many continue to conflate Bitcoin with cryptocurrencies, but those arguments can be dismantled, step by step.

This is an opinion editorial by Federico Rivi, an independent journalist and author of the Bitcoin Train newsletter.

Would you say that soccer and baseball are part of the same industry because both playing fields are covered with grass and in both games a ball is involved? Would you say that Bitcoin and cryptocurrencies are part of the same industry just because they are both in the digital realm and cryptography is involved in both?

The analogy is obvious but still too many equate Bitcoin with cryptocurrencies, refusing to see the substantial differences. The latest example comes from the Financial Times, whose columnist, Jemima Kelly, wrote that “Bitcoin can’t be separated from crypto.” Kelly is no stranger to criticism of Bitcoin — back in 2015, she highlighted the fall in the price of bitcoin from $500 to $300 — but this does not mean that her articles are not worth analyzing in detail, even more so when published in major newspapers such as the Financial Times.

So, “Bitcoin can’t be separated from crypto,” but why? Kelly provides a list of poorly-argued reasons that are worth dismantling.

Ponzi Schemes And The Criteria Of Money

“It doesn’t matter what bitcoin’s origins were — the people who push it now have the same financial incentives as those pushing any other crypto token. Satoshi Nakamoto, the creator of bitcoin, might have intended it to be used as money, but that does not make it so — it fulfills none of the necessary criteria, and instead operates in a pyramid-shaped structure that relies on constantly recruiting new members.”

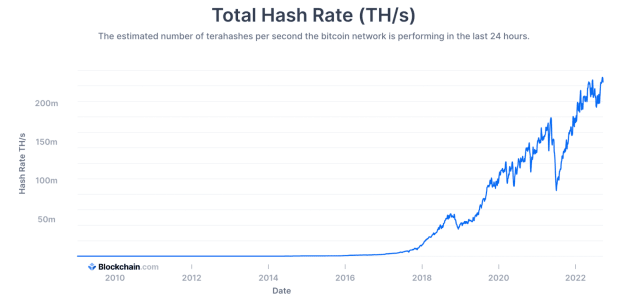

Pyramid schemes are, by definition, structures that can only stand as long as new investors keep coming in to pay interest to the first ones, i.e., those higher up in the pyramid. The moment no new funds enter, the structure collapses. Kelly fails to explain in what way Bitcoin would collapse without new investors. In fact, we are in the midst of a bear market that started 10 months ago with loads of money flowing out of bitcoin. In such a scenario, the pyramid scheme should have collapsed by now. As I write, however, Bitcoin is still the most widely distributed network on the planet and its hash rate is at an all-time high.

Bitcoin works with and without new funds coming in every day and this is a key difference with the “crypto” world, in which rug pulls happen on a regular basis, as the website rekt.news reports.

As for the criteria of money, Kelly forgets to specify what these are and how Bitcoin does not fulfill any of them. Although there is no universal consensus on how many key features money has, we can limit ourselves to highlighting the five main ones: store of value, medium of exchange, transportable, divisible, unit of account.

- Store of value: As inflation can be defined as devaluation due to monetary expansion, Bitcoin is technically and precisely a protection against inflation because of its fixed supply. It is even better than gold — the world’s most important store of value — in terms of stock-to-flow ratio, and it is therefore undoubtedly an excellent store of value.

- Medium of exchange: Although in Bitcoin’s history, scalability has created quite a few scars, today we are fortunate to have a protocol at our disposal that makes Bitcoin the best way to send money from one part of the world to another instantaneously and with almost non-existent fees. The Lightning Network is exactly what Bitcoin needed to become a medium of exchange.

- Transportability: Bitcoin is digital, anything to add?

- Divisibility: One bitcoin is divisible into 100 million sats. The Lightning Network also supports millisats, so one bitcoin can be divisible into 100 billion units. Try that with dollars.

- Unit of account: This is the only feature not yet achieved in Western economies because of bitcoin’s volatility, due to its ongoing price discovery phase that is likely to last for a few more decades. However, this does not mean that bitcoin is not already a much more reliable unit of account in many developing countries, where local currencies have fallen into hyperinflationary spirals.

Decentralization FUD

“Bitcoin is not in fact decentralised — not only do miners group together to form ‘mining pools’ but wealth is also hugely concentrated. On Tuesday, MicroStrategy announced that it had bought another 301 bitcoins, meaning this company alone now holds almost 0.7 per cent of the entire supply.”

Mining pools are not football teams and there are three considerations that Kelly omitted:

- Individual miners can break away from one pool and join another at any time should they feel that one is gaining too much power.

- If, until now, there has been the danger of transactions being censored by a pool — since it is the pool that writes the candidate block and can therefore theoretically choose which transactions to include and which to exclude — with Stratum V2 this problem is being resolved because each individual miner will be able to write its own candidate block. In the end, pools are groups of individuals acting for their individual interests.

- However undesirable it may be, a large hash rate controlled by a single miner does not give any power over the rules of the protocol, which are enforced by the individual nodes in the network, as demonstrated in the Blocksize War and in the beauty of proof of work.

As for MicroStrategy, Kelly has probably made a misguided analogy with the fiat world, where power and money go hand in hand. There, wealth and the ability to influence the rules of the system are directly proportional, a bit like in the proof-of-stake system, which is nothing but the crypto transposition of the current world. In Bitcoin, things work differently: as long as an individual runs a full Bitcoin node in a remote village in Kenya, even without holding any bitcoin, they have exactly the same amount of power that MicroStrategy has over Bitcoin (only if the company runs a full node, obviously — otherwise the individual has more power).

Innovation And Energy FUD

“…a ‘first-mover advantage’ does not always last. Other crypto tokens already have various features that bitcoin does not, and there has been renewed talk of a ‘flippening’, in which Ethereum’s value overtakes that of bitcoin due to the former’s switch to a less carbon-intensive form of mining.”

What exactly these features might be is not specified. Maybe smart contracts? It would be enough to study what is happening with the layers following Bitcoin’s blockchain: the Lightning Network, RGB, Taro, Fedimint, Liquid, OmniBolt, Sphinx and tbDEX, just to name the best known.

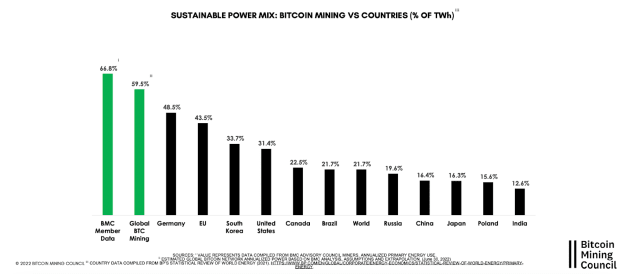

As for “carbon-intensive” mining, a lot of pages could be filled to disprove this idea. For the sake of this article, I will just show the data from the latest report by the Bitcoin Mining Council, which in July found that 59.5% of the energy used by the Bitcoin network comes from renewable sources, and that although Bitcoin consumes 0.15% of the energy produced globally, it is responsible for only 0.086% of CO2 emissions, and is therefore much greener than the average global production of goods and services. This trend will continue, given the incentive of miners to use low-cost energy sources. As Nic Carter put it: “Bitcoin mining is converging with the energy sector with amazing rapidity, yielding an explosion of innovation that will both decarbonize Bitcoin in the medium term, and will dramatically benefit increasingly renewable grids.”

The idea that the first-mover advantage does not last forever is also wrong. There is one key fundamental feature that allows Bitcoin to enjoy this constant advantage: scarcity or, to be more precise, finiteness. Bitcoin is finite, cryptocurrencies are not. And even if one were to use Bitcoin’s code by creating an identical copy, the first Bitcoin would be the original one: scarcity cannot be re-created once it has been discovered.

How Many Bitcoins? (Spoiler: Just One)

“Finally, there is not even agreement on what bitcoin is. For the vast majority it is the digital coin also known as ‘BTC’, currently changing hands at around $19,000. But there are other versions that have split off, such as the one promoted by Craig Wright, the man who claims to be Satoshi and who says BTC is a scam”.

This is a highly-contradictory sentence. If the “vast majority” agrees that Bitcoin is one thing, then there is an agreement, even if some megalomaniac with almost no following calls himself Satoshi Nakamoto and wants his token to be considered the real bitcoin. And in any case, when it comes to Bitcoin, where there is no single authority to provide certificates of authenticity, there is always a final judge: the market. Indeed, BTC is agreed upon by the free market, although many Western countries have now forgotten what that is.

This is a guest post by Federico Rivi. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc or Bitcoin Magazine.